Buy and Sell Homes with Local Experts You Can Trust

News & Market Trends

You’ll find our blog to be a wealth of information, covering everything from local market statistics and home values to community happenings. That’s because we care about the community and want to help you find your place in it. Please reach out if you have any questions at all. We’d love to talk with you!

There’s no denying the long-term financial benefits of owning a home, but today’s housing market may have you wondering if now’s still the time to buy. While the financial aspects of homeownership are important, the non-financial and emotional reasons are too. Here’s why.

The word home truly means something different to everyone. Whether it’s sharing memories with loved ones around the kitchen table or settling in to read a book in your favorite chair, the emotional connections we have to our homes can be just as important as the financial ones. Here are some of the things that turn a house into a happy home.

1. You Can Be Proud of Your Accomplishment

Buying a home is a major life milestone. Whether you’re ready to buy your first home or your fifth, congratulations will be in order once you’ve achieved your goal. The sense of accomplishment you’ll feel at the end of your journey will truly make your home feel like your special place. Go ahead and smile – you’ve earned it.

2. You Have Your Own Designated Happy Place

Owning your home offers not only safety and security, but also a comfortable place where you can relax and unwind after a long day. Sometimes that’s just what you need to feel refreshed and recharged.

3. You Can Find the Space To Meet Your Needs

Whether you want more room for your changing lifestyle (like a large backyard for entertaining or room for a home office) or you simply want to move closer to your loved ones, you can invest in a home that truly works for your evolving needs.

4. You Can Customize Your Surroundings

Looking to try one of those decorative wall treatments you saw online? Tired of paying an additional pet deposit for your apartment building? Or maybe you want to create an in-house yoga studio. You can do these things and much more when you own your home.

Bottom Line

Whether you’re planning to buy your first home, or you’re ready to move into a different one to meet your changing needs, think about the emotional benefits that can turn a house into a happy home. When you’re ready to make a move, connect with a local real estate advisor.

As the new year approaches, the idea of buying a home might be on your mind. It’s an exciting goal to set, and it’s never too early to start laying the groundwork. One crucial step to prepare for homeownership is building a solid credit score.

Lenders review your credit to assess your ability to make payments on time, pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from CNBCexplains:

“When it comes to mortgages, a higher credit score can save you thousands of dollars in the long run. This is because your credit score directly impacts your mortgage rate, which determines the amount of interest you’ll pay over the life of the loan.”

This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today.

According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. An article from Business Insiderexplains generally how your FICO score range can make an impact:

“. . . you don’t need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you’re wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experianhighlights some things you may want to focus on:

Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

Credit Applications: If you’re looking to buy something, don’t apply for additional credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score.

A lender will help you navigate the process from start to finish, from assessing which range your score falls in to telling you more about the specifics for each loan type.

Bottom Line

As you set your sights on buying a home in the upcoming year, a focus on boosting your credit score could help you get a better mortgage rate when the time comes. If you want to learn more, connect with a trusted lender.

If you’re planning to buy a home, knowing what to budget for and how to save may sound intimidating – but it doesn’t have to be. One way to ease those concerns is to make sure you understand some of the costs you may encounter up front. And to do that, always turn to trusted real estate professionals. They can help you set a plan and take a strategic look at your budget and your process before you even get started.

Here are just a few things experts say you should be thinking about.

1. Down Payment

Saving for your down payment is likely top of mind as you set out to buy a home. But do you know how much you’ll need? While every buyer’s situation is different, there’s a common misconception that putting 20% of the purchase price down is required. An article from the Mortgage Reportsexplains why that’s not always the case:

“The idea that you have to put 20% down on a house is a myth. . . . The right amount depends on your current savings and your home buying goals.”

To understand your options, partner with trusted real estate professionals to go over the various loan types, down payment assistance programs, and what each one requires. The more you know ahead of time, the easier the process will be.

2. Closing Costs

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various parties involved in your transaction. Bankrateexplains:

“Closing costs are the fees you pay when finalizing a real estate transaction, whether you’re refinancing a mortgage or buying a new home. These costs can amount to 2 to 5 percent of the mortgage so it’s important to be financially prepared for this expense.”

The best way to understand what you’ll need at the closing table is to work with a trusted lender. They can provide you with answers to the questions you might have.

3. Earnest Money Deposit

If you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). An EMD is money you pay as a show of good faith when you make an offer on a house. According to Realtor.com, it’s usually between 1% and 2% of the total home price.

This deposit works like a credit. It’s not an added expense – it’s paying a portion of your costs upfront. You’re using some of the money you’ve already saved for your purchase to show the seller you’re committed and serious about buying their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, an EMD isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your local area. They’ll advise you on what moves you should make so you can make the best possible decisions throughout the buying process.

Bottom Line

When buying a home, being informed about what to save for is key. Partner with a local real estate advisor so you’ll have an expert on your side to answer any questions you have along the way.

If you’re thinking about retirement or have already retired this year, it’s a good time to consider if your current house is still a good fit for the next chapter in your life.

Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about as you decide whether or not to sell and make a move.

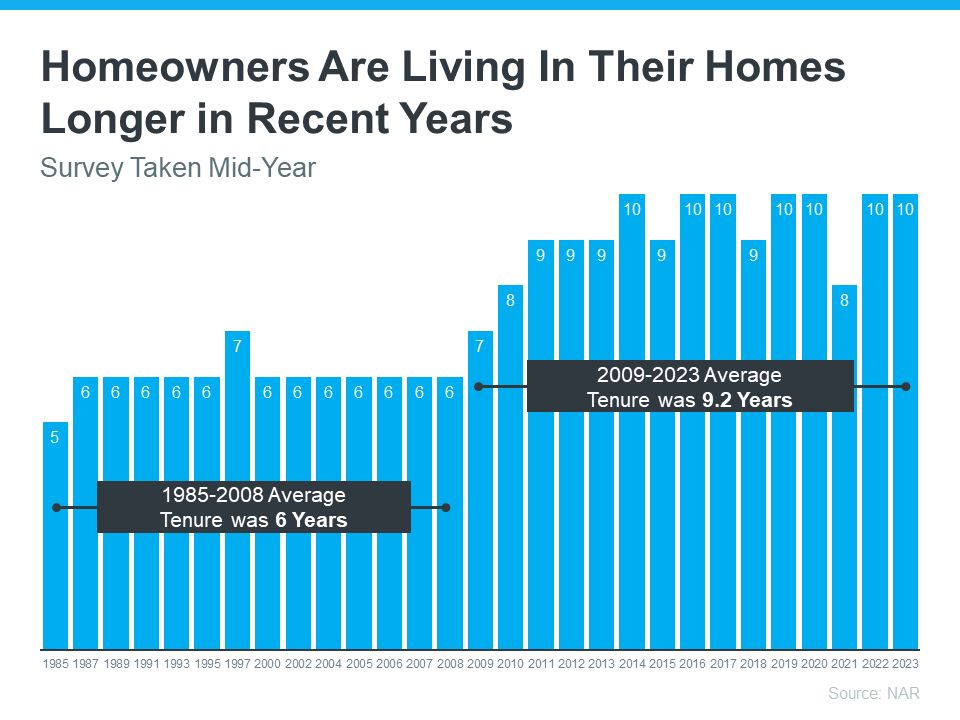

How Long You’ve Been in Your Home

From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):

When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

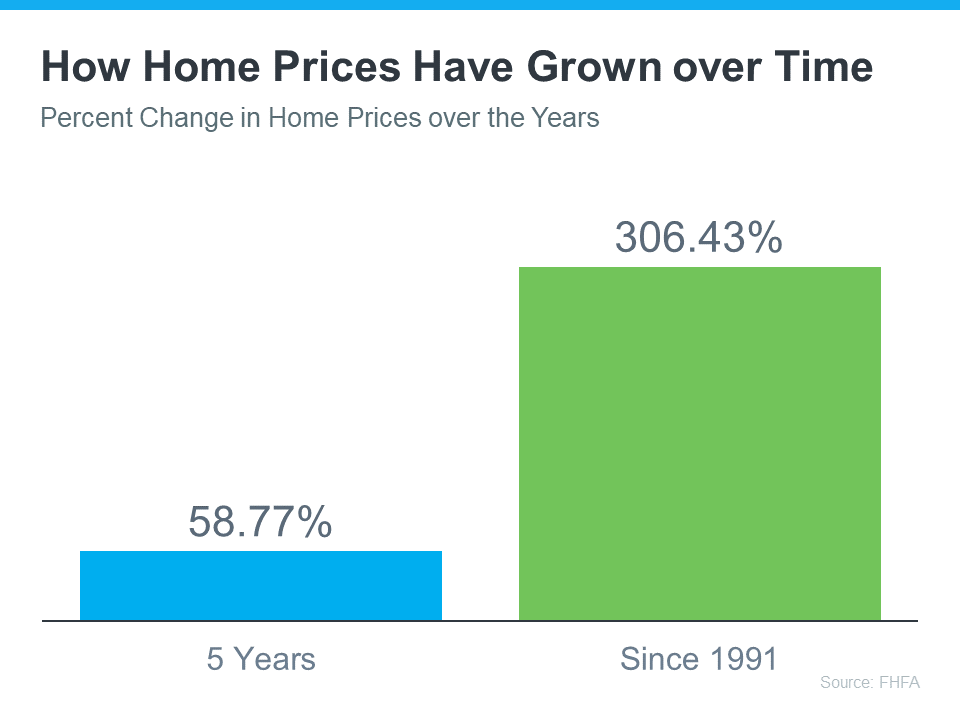

How Much Equity You’ve Gained

Additionally, if you’ve been in your house for more than a few years, you’ve likely built-up significant equity that can fuel your next move. That’s because the longer you’ve been in your house, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home since 1991 saw it more than triple in value over that time.

Consider Your Retirement Goals

Whether you’re looking to downsize, relocate to a dream destination, or simply be closer to loved ones, your home equity can be a key to realizing your homeownership goals. NARshares that for recent home sellers, the primary reason to move was to be closer to loved ones.

Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you through buying the home that’s right for your lifestyle today.

Bottom Line

Retirement can bring about major changes in your life, including what you need from your home. Connect with a local real estate agent to explore the available homes in your area.

When you read about the housing market, you’ll probably come across some information about inflation or recent decisions made by the Federal Reserve (the Fed). But how do those two things impact you and your homebuying plans? Here’s what you need to know.

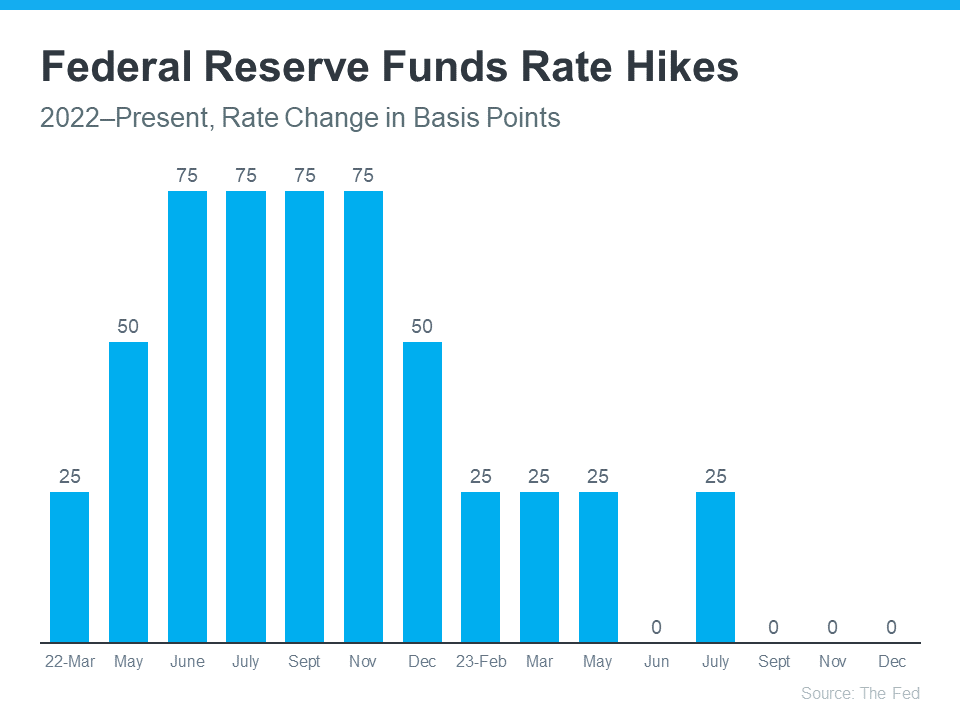

The Federal Funds Rate Hikes Have Stalled

One of the Fed’s primary goals is to lower inflation. In order to do that, they started raising the Federal Funds Rate to slow down the economy. Even though this doesn’t directly dictate what happens with mortgage rates, it does have an impact.

Recently inflation has started to cool, a signal those increases worked and are bringing inflation back down. As a result, the Fed’s hikes have gotten smaller and less frequent. In fact, there haven’t been any increases since July (see graph below):

And not only has the Fed decided not to raise the Federal Funds Rate the last three times the committee met, they’ve signaled there may actually be rate cuts coming in 2024. According to the New York Times (NYT):

“Federal Reserve officials left interest rates unchanged in their final policy decision of 2023 and forecast that they will cut borrowing costs three times in the coming year, a sign that the central bank is shifting toward the next phase in its fight against rapid inflation.”

This indicates the Fed thinks the economy and inflation are improving. Why does that matter to you and your plans to buy a home? It could end up leading to lower mortgage rates and improved affordability.

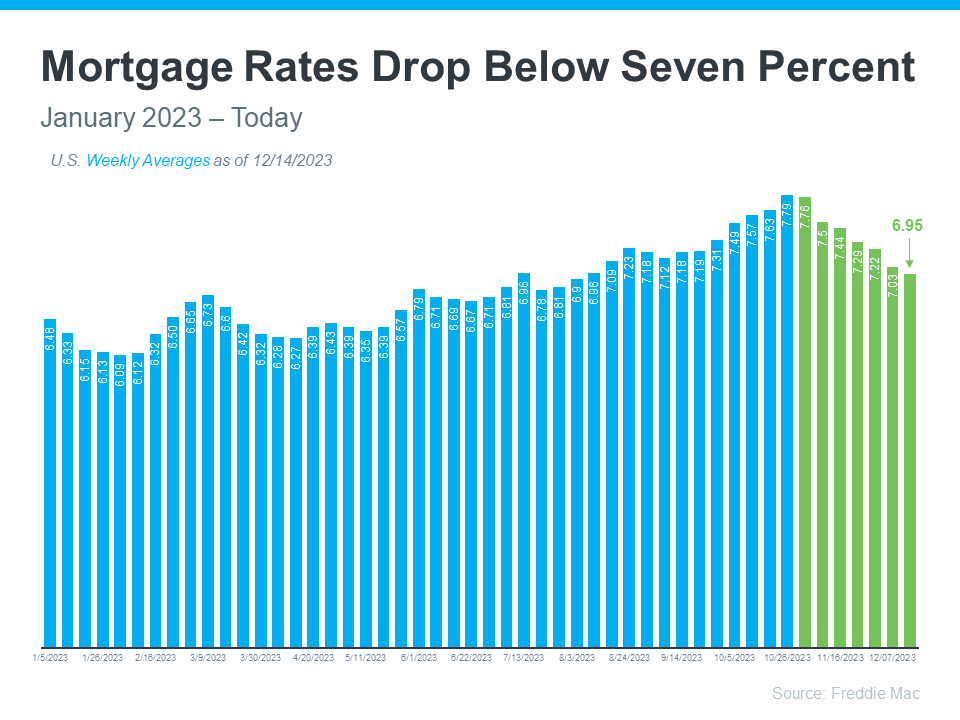

Mortgage Rates Are Coming Down

Mortgage rates are influenced by a wide variety of factors, and inflation and the Fed’s actions (or as has been the case recently, inaction) play a big role. Now that the Fed has paused the increases, it looks more likely mortgage rates will continue their downward trend (see graph below):

Although mortgage rates may remain volatile, their recent trend combined with expert forecasts indicate they could continue to go down in 2024. That would improve affordability for buyers and make it easier for sellers to move since they won’t feel as locked-in to their current, low mortgage rate.

Bottom Line

The Fed’s decisions have an indirect impact on mortgage rates. By not raising the Federal Funds Rate, mortgage rates are likely to continue declining. Rely on a trustworthy real estate expert to give you expert advice about changes in the housing market and how they affect you.

If you’re thinking about selling your house on your own, called “For Sale by Owner” or FSBO, there are some important things to consider. Going this route means taking on a lot of responsibilities by yourself – and that can be a bit of a headache.

A recent report from the National Association of Realtors (NAR) found two of the most difficult tasks for people who sell their house on their own are getting the price right and understanding and performing paperwork.

Here are just a few of the ways an agent helps with those difficult tasks.

Getting the Price Right

Setting the right price for your house is important when you’re trying to sell it. If you’re selling your house on your own, two common issues can happen. For starters, you might ask for too much money (overpricing). Alternatively, you might not ask for enough (underpricing). Either can make it hard to sell your house. According to NerdWallet:

“When selling a home, first impressions matter. Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing.

. . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

To avoid these problems, it’s a good idea to team up with a real estate agent. Real estate agents know how to figure out the perfect price because they understand the local housing market. They can use their expertise to set a price that matches what buyers are willing to pay, giving your house the best chance to impress from the start.

Understanding and Performing Paperwork

Selling a house involves a bunch of paperwork and legal documentation that has to be just right. There are a lot of rules and regulations to follow, making it a bit tricky for homeowners to manage everything on their own. Without a pro by your side, you could end up facing liability risks and legal complications.

Real estate agents are experts in all the contracts and paperwork needed for selling a house. They know the rules and can guide you through it all, reducing the chance of mistakes that might lead to legal problems or delays.

So, instead of dealing with the growing pile of documents on your own, team up with an agent who can be your advisor, helping you avoid any legal bumps in the road.

Bottom Line

Selling your house is a big deal, and it can be complicated. Having a real estate agent can make a huge difference in setting the right price and managing all the details so you can sell confidently. Connect with a local real estate agent to make the process smooth and take the stress off your plate.

Many want to realize their dream of owning a home. It takes some effort too. You must save and have a good credit score. While hoping for the best, issues of life may hinder your dreams. Sometimes you lose your job or fall sick, plunging yourself into more debt.

California residents have a little glimpse of light regarding home loan issues. But lenders can take action against mortgage defaulters. In that case, what options do you have as a homeowner?

If you default on a mortgage payment, you can opt for foreclosure or short sale. Though you may lose your home during the process, the consequences differ. So, read our analysis on foreclosure vs. short sale in California.

Understanding Short Sales

If you sell your house for a value that is less than your loan debt, the transaction is a short sale. Before you engage in a short sale, you must get your mortgage lender’s approval.

A short sale can cause your lender, typically a bank, to lose money. So, they must see the reasons why it makes sense.

What Qualifies You for a Short Sale?

You must show evidence of financial hardship to qualify for a short sale, and your documents should spell cases like job loss, ill health, or natural disaster, to name a few. Make sure that your lender accepts these reasons. Otherwise, you can’t proceed with a short sale.

In addition, you must provide your lender with the most recent selling prices of homes in your neighborhood. These are typically called comps, or comparable sales.

Your creditor will check your documents and real estate price data. If accepted, then you can sell your home under short sale. In this case, your lender might not recoup the full mortgage debt value.

How Does a Short Sale Affect Your Credit Score?

Your credit score will drop by 50 points if you repay your loan on time after completing your short sale transaction. If paying late, your credit score can drop by 200 points.

Borrowers with a low credit score of 700 and less pay higher rates. Likewise, those with higher credit scores enjoy lower rates and better chances of getting loans.

How Long Does It Take To Get a Mortgage Loan After a Short Sale?

After a short sale, it takes about two to four years to get another home loan. Your home worth also determines how soon you can secure a new loan.

For instance, if your creditors lost 20 percent of their loan amount, the next mortgage becomes available in two years. Meanwhile, it takes four years before a new loan for a 10 percent drop in debt value.

Understanding Foreclosures

Foreclosures empower the lender to take over your home if you stop making payments. Since you used your home as collateral, whether it’s worth the debt, the bank can seize it.

Your creditor will notify you about the default 30 days after failing to repay. If you don’t attempt to pay, expect a foreclosure notice from your lender. Of course, that means you will lose your home.

How Does Foreclosure Affect Your Credit Score?

California has its procedures, consequences, and length of time for foreclosures. According to FICO, your credit score can drop up to 100 to 200 points, which means foreclosure has a more severe effect on your credit score than a short sale.

How Long Does It Take To Get a Mortgage Loan After a Foreclosure?

Besides taking an enormous toll on your credit score, you may wait for seven years before securing another home loan. Depending on why your income dropped, some financial institutions can give you a loan within a shorter period.

When applying for a new mortgage, inform your prospective lender that you already had a foreclosure.

With Foreclosure vs. Short Sale, Which Option Should You Take?

Homeowners in California enjoy certain rights that prevent lenders from coming against them in a full sweep. No matter how favorable the law is, it doesn’t take away the creditor’s power. So, let’s examine both foreclosure and short sale options to help you choose which is better.

When to Exit Your Property

Check your deed of trust for the power that allows lenders to come to your home. You can stay in your home for a while since it takes months before the court actions on your lender’s request.

You will get a notification from your bank on the date of the sale, and it takes 20 days from the date you received the notice. Your lender will also notify you after selling your house. At that time, get ready to leave your property within 3 to 45 days after getting the notice.

If your creditor files for a deficiency judgment, you can get your house again within one year. But the court order also mandates you to pay the difference between the outstanding debt and the sale price.

Redeeming Your House

If you have no way of getting your house back, go for a non-judicial foreclosure. Remember, only a deficiency judgment can make your home redeemable, and otherwise, you cannot reclaim it once the transaction window closes.

Know Your Type of Mortgage to Avoid Tax Implications

If you have a non-recourse loan, you shouldn’t pay a fine for the difference between the total debt and the sale amount. But you will pay tax for the same reasons in a recourse loan.

A Short Sale Is Faster

A short sale offers you the opportunity to sell your property for less than your mortgage. Remember to secure your lender’s approval to initiate a quick sale. As a positive, California laws mandate financial institutions to respond on time. So, typically you can complete the deal within six months.

No Deficiency Judgment Against Short Sales

In California, the law prevents financial institutions from getting deficiency orders against mortgage defaulters for the difference between the short sale amount and the debt owed. But expect your credit score to reduce after completing your transaction.

Find out which markets are hot and what sellers are looking for in their new hometowns.

According to the 2020 Atlas Van Lines Migrations Patterns Study of 65,000 interstate and cross-border moves, traditional population centers in the US are giving way to areas that put a priority on affordability, home options, and, perhaps most importantly, wide-open spaces with room to roam. Here are the states where everyone will be living next.

Idaho (66.4 percent)

We hear so much about people heading south for warmer weather and increased job opportunities. Therefore, it might come as a surprise that Idaho tops the list of inbound moves according to the Atlas study. This is due to a number of factors, including Idaho’s proximity to California, which made up 57.1% of outbound moves according to the same study.

What Idaho lacks in sunny days and coastline it makes up for in many of the factors that draw in new residents — safety, price, and job opportunities. Here you’ll find a low cost of living and low insurance rates, especially compared to some of its more expensive neighbors. With low unemployment levels, Idaho is a great place to find a job, especially if you’re in the medical or tech field. According to the Bureau of Labor Statistics, these groups make up the highest-paid employees in the state.

North Carolina (64.6 percent)

It seems that everyone is moving to North Carolina, and with so many great options it’s no wonder. From the big-city living you’ll find in Charlotte to the hipster meccas of Greensboro and Asheville to the Raleigh-Durham Research Triangle, North Carolina offers sophisticated living at a fraction of the price you’ll pay in other states with major metropolitan areas.

Besides educational and job opportunities, North Carolina offers greater affordability than other areas along with plenty of perks. While you’ll experience milder weather throughout much of the year, you’ll still experience four distinct seasons, something that’s missing in many other southern states. In addition, there’s greater diversity and a more international flavor here so newcomers will feel right at home.

Maine (62.4 percent)

Folks are moving to Maine in record numbers, making it tough to find homes to buy or rent in some areas. Why? In large part because of the lower cost of living you’ll find, where even homes with lots of land are going for less than a starter home in other states. In addition, Maine’s emphasis on the natural world and outdoor adventure makes it attractive for young, active residents — especially those who are environmentally conscious and able to work remotely.

New Hampshire (61.6 percent)

Similarly, New Hampshire’s reputation for year-round outdoor beauty and active living options in the area’s ski resorts, lakes, and forests make it an exciting setting for young residents looking to get away from life in the big city. However, there’s still close proximity to major employment hubs throughout the Northeast plus no income or sales tax, contributing to increased affordability.

Alabama (60.8 percent)

Alabama is a popular destination for young professionals and retirees, with residential options ranging from big cities to suburban luxury enclaves to coastal retirement communities. In addition, there’s year-round warm weather without the crowds you’ll find in Florida and Texas. Even without pro sports teams and some of the advantages of nearby Tennessee and Georgia, Alabama’s college football culture and historical sites offer plenty of opportunities for fun and adventure.

District of Columbia (60.2 percent)

The mid-Atlantic region offers exceptional living with mild year-round weather and proximity to major employment hubs. However, its popularity has resulted in long commutes plus skyrocketing home prices and tax rates in Virginia and Maryland. That may be why so many people are flocking to the relatively more affordable DC neighborhoods. Here you’ll find everything from historic homes in Georgetown to new construction condos in newly hip in-town neighborhoods. In addition, Amazon’s investment in the area is bringing in a host of residents who are finding a new hometown in the District.

New Mexico (60.0 percent)

Like Idaho, New Mexico is the new home for many of the California residents fleeing the state. Here you’ll find a combination of residential affordability and plenty of elbow room. Newcomers are also finding lower costs of living and lower housing prices along with a growing job market. On top of all of that, there’s a reason New Mexico is called “The Land of Enchantment” as the state’s many natural beauties continue to enchant newcomers.

Nevada (59.8 percent)

After struggling in the aftermath of the 2008 mortgage crisis, Nevada has rebounded in a big way to become one of the country’s most popular destinations for new residents. Here there are many job opportunities, low taxes, and a lower cost of living than you’ll find in other western states. In addition, you’ll find plenty of room for outdoor activities and plenty of space for new neighborhoods to accommodate all of those incoming residents.

Alaska (58.6 percent)

Speaking of wide-open spaces, Alaska offers some of the world’s most extraordinary outdoor vistas and sporting opportunities. With incentives to offset the cost of moving, lower housing prices, and no state income or sales tax, Alaska offers more affordability than many other places in the Lower 48. In addition, for young people who are looking to live a life of adventure while maintaining their professional options through remote work, Alaska offers an ideal setting.

Kentucky (57.7 percent)

One of the biggest outcomes of the pandemic has been the ability to work from anywhere — a trend that has been accelerated by work-from-home policies from some of the country’s biggest employers. This has been great news for states like Kentucky, which offer lower costs, plenty of space to build or expand, and beautiful outdoor scenery. In addition, the state is home to hip enclaves like Louisville where you’ll find arts, culture, museums, and history alongside craft bourbon distilleries and Churchill Downs, the home of the Derby.

Wherever you’re moving next, a fast and convenient home sale process will make the transition easier. Reach out to us at Offercity for a free, no-obligation evaluation of your property. Let us help you move to your new favorite state on your terms and your timeline.

Selling a home for the first time can feel just as daunting as going through the initial home-buying process. You may not be sure how to price it, what needs fixing beforehand, and what other tasks are necessary to get your home sold for a worthwhile profit. If you’ve found yourself wondering, “should I sell my house”? It’s time to check out some of the best advice from Offercity.

Determine Your Home’s Worth

You can’t just set an arbitrary selling price. You need to look at the housing market in your area, consider the costs of similar homes, and get an accurate determination of your home’s potential worth.

Having an accurate selling price can help you sell your home more quickly than if you had a cost set far beyond what anyone would be willing to pay. You may even consider paying for an appraisal to help you determine the best price to set.

You can check out real estate sites to get some of this information. Find homes recently sold in your neighborhood or within the same city. Make sure the number of bedrooms and bathrooms match and find similarities with amenities and unique offerings, such as a pool if you have one. The more similar the listings, the more likely you are to find a suitable number.

Learn About Equity

If your home has no equity, you aren’t going to make a profit. You need to learn about your home’s equity to determine if it’s a good time to sell. Home equity is the remaining value after taking away what is owed to your mortgage lender. If your entire sale price needs to go toward your remaining mortgage payments, you’ll have no money left to settle closing costs or put a down payment on your next home.

The best advice is to be sure you have enough equity to cover the remaining mortgage and any closing costs and a 20% down payment for your next home purchase. Without this, it may be difficult to purchase your next place. Most people do not have enough equity in their home until they’ve lived there and paid into their mortgage for five years or more.

To determine your potential equity, take your remaining mortgage amount and subtract it from your home’s worth (or potential selling price). If you hope to buy a larger house, the number will need to be substantial. You won’t need as high of a number if you’re looking to downsize.

Discover the Cost of Selling

Selling your home isn’t free. There are always costs involved with everything you do, and selling your home is no different. The repairs you need to make, to make the home livable and worthwhile to a potential buyer can add up quickly. You also need to consider what final closing costs you’ll have to cover or if you can get the buyer to handle them.

Set Your Sale Timeline

On average, sellers see their homes sold within just two months since they put them on the market. However, this number can vary widely. It all depends on how quickly you can get things in order and how quickly you are willing to be out of there. You can set your sale timeline if you need more time to make repairs, get your belongings out of the home, and find your next place to live.

The timeline also starts a little sooner for most than the day of listing. Many people take a good couple of months to make the changes necessary and have their staging photos taken. This prep time should also be accounted for when you’re considering selling. The more time and money you can spend on getting the home updated and in proper order, the more you may be able to list it for when it comes time.

Decide on Your Method of Selling

If you’re also struggling with the question of “how should I sell my house,” it’s wise to consider the choices. Working with a real estate agent is the most common method of selling a home. The real estate agent has the experience and knowledge to get you through the process easily. However, there are three other options for selling a house without the need for a real estate agent at all. These methods are:

Selling your home with the help of a real estate agent to interested parties in the area can help you earn a worthwhile profit. However, you’ll also need to pay extra fees that aren’t involved with the other options. Selling by owner allows you to take the lead, but it puts all the work on your shoulders.

Selling to property investors or an iBuyer are valid solutions if you’re looking to make a fast sale and avoid the staging photos and strangers traipsing in and out of your place while still living there. Overall, though, the solution you choose needs to be what is the most beneficial to you. Everyone will choose differently.

Offercity Can Help Answer ‘Should I Sell My House’

Offercity is a great option for homeowners looking to sell their homes quickly and for the best price. Sellers don’t have to worry about decluttering, making costly repairs, home inspections, or paying fees or commissions. We work on behalf of sellers by marketing homes directly to local investors. Investors bid on these homes, therefore, guaranteeing the best possible as-is cash offer for the seller. Contact us to get started.

If you’re gearing up for retirement, these are the best cities for your next home.

Southern California is one of the most iconic regions in the United States. From movies to music and television, this area has been heralded for its sunshine, surfing, and easy-going vibe, making it a perfect choice for retirement. Whether you’re planning a retirement that’s focused on golf and tennis, long walks on the beach, or a second-act career reboot, you’ll find a world of options when you retire in Southern California.

SoCal has almost too many amazing towns and cities to count and it’s important to remember that many areas offer access to multiple cities. In addition, with easy travel options between the different communities, you’ll enjoy the opportunity to visit your favorite areas frequently. Alternatively, consider splitting your time between different communities with a variety of desirable features.

Palm Springs

There may be no Southern California community so effortlessly cool as Palm Springs. Made up of a number of smaller communities, including Palm Desert, Indio, Palm Springs, Desert Hot Springs, La Quinta, and Indian Wells, this is an area that combines quintessential California architectural and design features with a world-class culinary scene and an emphasis on the arts to create a true playground for grown-ups — and a picture-perfect setting for your retirement.

Fans of mid-century modern styles will find swoon-worthy homes and interior designs. As an ultra-cool playground for the rich and famous, there’s no shortage of luxurious amenities and recreational options. Those who are looking for an active, outdoor lifestyle will find golf, hiking, and swimming while spas, gardens and museums appeal to those seeking relaxation.

Santa Barbara

Nestled between the Pacific Ocean and the Santa Ynez Mountains, Santa Barbara is a true paradise, offering spectacular scenic vistas and year-round great weather. Named for a Presidio dating back to the era of Spanish Conquest, Santa Barbara still pays tribute to its historic past. Here you’ll find residential architecture ranging from authentic Victorian homes to Mediterranean Revival, Spanish Colonial Revival and Mission Revival styles.

If you’ve been thinking about going back to school after you retire, you’ll find plenty of options in Santa Barbara. The city is host to four major institutions of higher education, including the University of California Santa Barbara, Santa Barbara City College, Westmont College, and Antioch University. Spend time in the area’s parks, stroll the picture-perfect beaches and hiking trails, or hit the links at some of the country’s best-known local golf courses.

Pasadena

Popularly referred to as the City of Roses, Pasadena is probably best known as the home of the Rose Bowl and its iconic parade and college football tournament game airing each New Year’s Day. However, the other 364 days of the year, Pasadena offers spectacular natural and manmade beauty, making it one of the most beguiling and unforgettable cities in Southern California.

If you want to be close to the big city while retaining a sense of small-town living, you’ll love Pasadena. While visitors come from all over the world to the area’s colleges and universities, its population is just over 140,000 making it relatively small by SoCal standards. As the home of CalTech, Pasadena is a great choice for those who are retiring after a career in high tech or engineering, especially if you’re planning to keep a hand in with consulting opportunities post-retirement.

Los Angeles

Of course, no list of Southern California cities would be complete without Los Angeles. As the center of the entertainment industry and a hub for business of all kinds on the west coast, LA is one of the most vibrant and exciting cities on earth. In addition, however, there are a wide variety of enclaves and neighborhoods in the surrounding metropolitan area for those who want to be near the city without actually living in the city.

Whatever you’re thinking about doing in retirement, you can find opportunities along with like-minded individuals. Start a business here and have access to some of the most important professional connections in the country. Go back to school and attend classes at exceptional colleges and universities. Pursue your long-delayed artistic dreams when you sign up for an improv or acting class and go out on auditions. Immerse yourself in the city’s artistic, cultural, and international life. The possibilities are truly limited only by your imagination.

San Diego

Located in Southern California along the border with Mexico, San Diego offers you everything you’re looking for and a combination of both a big-city lifestyle and exclusive resort-style gated enclaves. The metro area is made up of more than 100 distinct neighborhoods, allowing you to find the perfect location for your active retirement wherever you want to be. In addition, San Diego has one of the country’s best climates, with year-round mild weather enhancing the area’s natural scenery.

If you love outdoor living, San Diego is truly the place for you. Here you’ll experience everything from year-round golf to one of the most bird-friendly areas in the United States. There are nature preserves with rare plant species and one of the country’s most robustly diverse animal populations. You’ll also enjoy big-town arts, culture, sports, and entertainment, along with incredible views from the mountains to the area’s world-famous beaches.

If you’re ready to make a move, Offercity offers an unbeatable option for your home sale. If you’ve got equity in your home and want to avoid the hassles and expenses associated with a traditional home sale, we’ll bring you competing offers from multiple local real estate investors in your area. Not sure where you’re moving next? We’ve got you covered with variable terms for closing from 10-60 days, plus a cash advance of up to $10,000 to help you cover your expenses.

By continuing to use this site, you consent to our use of

technologies that

analyze and monitor activity on our website, may record your activity on this site, and sometimes provide you with

tailored advertising. You also consent to our Privacy

Policy

and Terms & Conditions